Qualified Domestic Limited Partner (“QDLP”) scheme has caused great sensation in the asset management market ever since it was initiated in Shanghai back in 2012. On one hand, it is an innovative pilot scheme; on the other hand, it is impressive that a great number of global asset managers have entered into China market through the QDLP scheme.

In recent years, improvement has been made on the eligibility requirements of QDLP fund manager and the application procedure of QDLP license, requirements for registration with AMAC have been made clearer, the form of QDLP funds has increased, more cities have kick-started pilot QDLP scheme and more foreign exchange quota has been approved, all of which have helped facilitate the QDLP business. However, QDLP fund managers have also been facing some challenges in the course of fundraising. In this spring, many financial sectors in China are speeding up their opening-up to foreign investors, and we would like to take this opportunity to introduce the QDLP business, especially the evolvement of relevant QDLP rules and our observations in the past projects.

Section 1 General Introduction

According to current foreign exchange regulations, investors in China have limited access to overseas financial markets, which mainly include the Qualified Domestic Institutional Investor (“QDII”) scheme started in 2006, QDLP scheme initiated in 2012, Stock Connect Program launched in 2014, Mutual Recognition of Funds between Mainland China and Hong Kong initiated in 2015, as well as the SSE-JPX ETF Connectivity scheme and Shanghai-London Stock Connect scheme established in 2019.

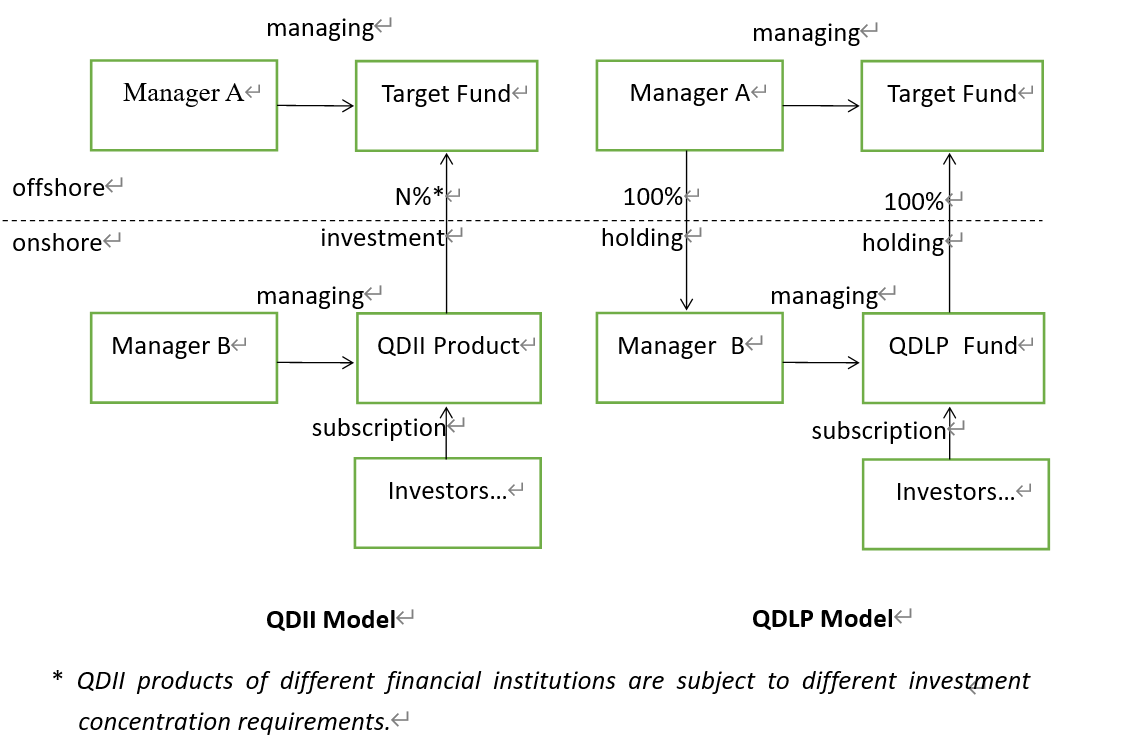

The QDLP scheme enables an institution with QDLP license and quota (i.e., the QDLP fund manager) to launch a QDLP fund by raising capital from qualified investors in China and invest in overseas financial markets with such capital after converting it into foreign currency within the quota approved.

- Advantage of QDLP Compared with QDII

Currently, QDII license and quota are only available to such financial institutions as mutual fund management companies and securities companies regulated by the China Securities Regulatory Commission (“CSRC”) and commercial banks, trust companies, insurance companies and insurance asset management companies regulated by the China Banking and Insurance Regulatory Commission. The QDLP fund manager is not required to hold any financial license, although it needs to register with the Asset Management Association of China (“AMAC”) as a private fund manager.

Through the QDII scheme, global asset managers may sell their funds to investors in China indirectly through asset management products (“QDII products”) of financial institutions with QDII license and quota, and some QDII products shall comply with relevant rules on investment concentration; whereas, through QDLP scheme, global asset managers may set up a fully owned subsidiary in China, which may launch a QDLP fund by raising capital in China and then invest such capital to overseas funds with a Feeder-Master investment structure.

QDLP funds may invest in securities investment funds (retail funds and hedge funds), and QDLP funds in some pilot cities are also allowed to invest in other funds such as PE funds. Generally speaking, QDII products are only allowed to invest in securities investment funds, and applicable rules on some QDII products impose even more stringent requirements (e.g., QDII products of securities companies and mutual fund management companies can only invest in retail funds, and QDII products of commercial banks are not allowed to invest in hedge funds).

Therefore, the QDLP scheme, considered an important supplement to the QDII scheme, is an important foreign investment channel for domestic investors.

- Pilot Cities

Since Shanghai initiated the QDLP scheme in 2012, many other cities have followed suit, including but not limited to Tianjin (2014) and Qingdao (2015). Shenzhen initiated Qualified Domestic Investment Enterprise (“QDIE”) scheme, a pilot scheme similar to QDLP, in 2014.

In 2019, the State Council approved Beijing’s endeavor to launch its QDLP scheme. With the support by the State Council, Beijing local financial regulator, local foreign exchange authority and other competent authorities jointly issued a 3-year action plan on the opening-up of its financial sectors, according to which QDLP scheme is scheduled to be launched by the end of December 2019. QDLP scheme in Beijing has attracted much attention recently.

Further to Beijing’s policy, various districts of Beijing have made their own efforts to attract investment by global asset managers. For example, according to a policy issued by Shunyi District of Beijing, it will recommend eligible institutions to apply for QDLP license and quota, and QDLP fund managers may choose one of the two financial subsidies:

- A QDLP fund manager will be awarded RMB 1 million, 2 million, 4 million, 6 million and 10 million respectively if the AUM of its QDLP funds reaches RMB 500 million, 1 billion, 2 billion, 3 billion and 5 billion, respectively.

- A QDLP fund manager will be subsidized in an amount up to 80% of its annual contribution to local finance authority within the first three years after its formation.

We understand that the pilot QDLP rules in Beijing will draw upon experiences from QDLP schemes in other cities, reflect the latest legislative development regarding private funds and contains certain unique features with respect to the eligibility requirements and permitted business scope of QDLP fund manager.

- Development of QDLP

Currently, Shanghai has the most established QDLP scheme, which has attracted around 30 global asset managers. The first batch of QDLP fund managers are all hedge fund managers (e.g., Man Group and Oak Tree) while the rest are mainly leading global asset managers (e.g., BlackRock and Morgan Stanley).

Shanghai amended its pilot QDLP rules in 2017 and relaxed restrictions in several aspects. For example, contractual funds are formally permitted in addition to funds in the form of limited partnership, PE funds and other funds are permitted as the investment target of QDLP funds in addition to securities investment funds, QDLP fund managers may be controlled either by foreign investors directly or through existing foreign-invested entities. With such policy development, around 20 global asset managers have set up companies and obtained QDLP licenses within only two years (i.e., 2018 and 2019).

In addition to wholly foreign owned QDLP fund managers, a joint venture mutual fund management company (i.e., China International) and a subsidiary of Guangfa Securities (i.e., GF-Persistent) also obtained QDLP license.

Tianjin amended its pilot QDLP rules as well, drawing upon experience from earlier QDLP schemes and reflecting latest legislative development of private funds.

Qingdao has promoted its QDLP scheme as one of the key measures on building the Qingdao Wealth Management Financial Comprehensive Reform Pilot Zone.

Shenzhen also learned from past experience and raised further requirements on improving overseas investment projects, investment scale, custodian bank and QDLP fund manager administration in 2017. After a few years, Shenzhen also has several institutions obtained the QDIE license and quota in 2018.

- Other Districts Expected to Initiate QDLP Scheme

In addition to Shanghai, Tianjin, Qingdao and Beijing, some other districts in China are expected to initiate pilot QDLP scheme, including Guangdong (QDLP), Guangxi (QDIE) and Shandong (QDLP), according to relevant policy documents issued by the State Council and the People’s Bank of China (“PBOC”).

Section 2 QDLP License

- Procedure

The QDLP scheme in all cities is generally administered by the local financial regulator, and supervised by the joint conference consisting of such local financial regulator, local administration for market regulation, commerce authority and foreign exchange authority etc. Taking Shanghai as an example, to apply for QDLP license and quota, the general procedure consists of three major steps:

Step One: Application to the joint conference, and obtaining pre-approval.

Step Two: Setting up company, including company name pre-approval and registration.

Step Three: Application to local financial regulator for QDLP license and quota.

The sequence of Step One and Step Two may be adjusted based on the actual circumstances.

- Improvement Brought by Foreign Investment Law

Foreign investment related policy has undergone major changes twice since QDLP scheme was initiated in 2012. In 2012, a case-by-case approval by local commerce authority was still required. In 2016, only a filing with local commerce authority was required if the foreign invested entity intended to engage in business outside the negative list. After the implementation of the Foreign Investment Law in 2020, there is no need to get approval by or to do filing with the local commerce authority, and foreign investors can register the company with local administration for market regulation directly and submit relevant information report concurrently.

Therefore, the establishment procedure of a QDLP fund manager has been continuously optimized in recent years.

Section 3 Quota

Quota is an issue not only with QDLP/QDIE scheme, but also with such regime as QDII. For example, the State Administration of Foreign Exchange (“SAFE”) revealed in a press conference in September 2016 that QDII quota, amounting to USD 90 billion, have been used up as of March 2015. Thereafter, it is not until April 2018 that SAFE resumed granting new QDII quota to financial institutions. Similarly, the development of QDLP business relies on foreign exchange quota as well.

- Recent Development on Quota

In April 2018, SAFE released news that it will advance QDLP and QDIE scheme steadily and increase the quota for each of the QDLP scheme in Shanghai and the QDIE scheme in Shenzhen to USD 5 billion respectively. Before that, we learned that Shanghai has used up the USD 2 billion quota as of the end of February 2018.

In June 2019, SAFE Administrator Mr. Pan said that one of the key tasks of SAFE recently is to push for transformation of QDLP business in Shanghai from a pilot scheme to a full-scale program. As the finance sectors are opening up to foreign investors rapidly, the whole industry expects that such aim will be achieved as soon as possible.

- Allocation of Quota

Taking QDLP in Shanghai as an example, QDLP license and quota in practice will be granted to QDLP fund managers at the same time. As of now, Shanghai has granted QDLP license and quota to applicants in several batches. Applicants of the same batch generally receive the same amount of quota. Generally, after the quota is used up, QDLP fund managers may apply for additional quota.

Section 4 Application of Polies at both State and Local Level

On one hand, the QDLP scheme is a local pilot scheme, and relevant cities have issued their own pilot rules (“pilot QDLP rules”); on the other hand, QDLP fund managers are private fund managers and QDLP funds are private funds, so that they are subject to national rules and regulations on private fund managers and private funds. Under such circumstances, regarding any issue, if the pilot QDLP rules (or the State rules) are silent, the provisions in the State rules (or the pilot QDLP rules) shall apply; while if the provisions in pilot QDLP rules and the State rules are contradicting, the more stringent rule shall apply.

For example, regarding contractual QDLP funds in Shanghai, the pilot QDLP rules only provide that capital raised shall not be less than RMB 30 million while there is no such minimum investment for each investor. Under such circumstances, the State rules shall apply. That is to say, according to the Interim Measures for the Supervision and Administration of Privately-Raised Investment Funds, the minimum subscription amount of each single investor shall not be less than RMB 1 million, with only a few exceptions for some certain categories of special investors.

Section 5 Registration as Private Fund Managers

QDLP fund managers are private fund managers. After obtaining QDLP license and before launching QDLP funds, QDLP fund managers shall register with the AMAC. In Shanghai, there are 28 QDLP fund managers that have registered with the AMAC so far.

- Types of Private Fund Managers

A private fund manager may choose to register as PE/VC fund manager, private securities investment fund manager, private asset allocation manager or other private fund manager after meeting relevant requirements. According to the specialized operation principle as requested by the AMAC, a private fund manager shall select only one from abovementioned four options.

As explained by AMAC on June 21, 2018, considering that QDLP funds may invest in overseas securities, PE products, alternative products or other products, QDLP fund managers may be registered as “other private fund managers”.

- Segregation with WFOE PFM

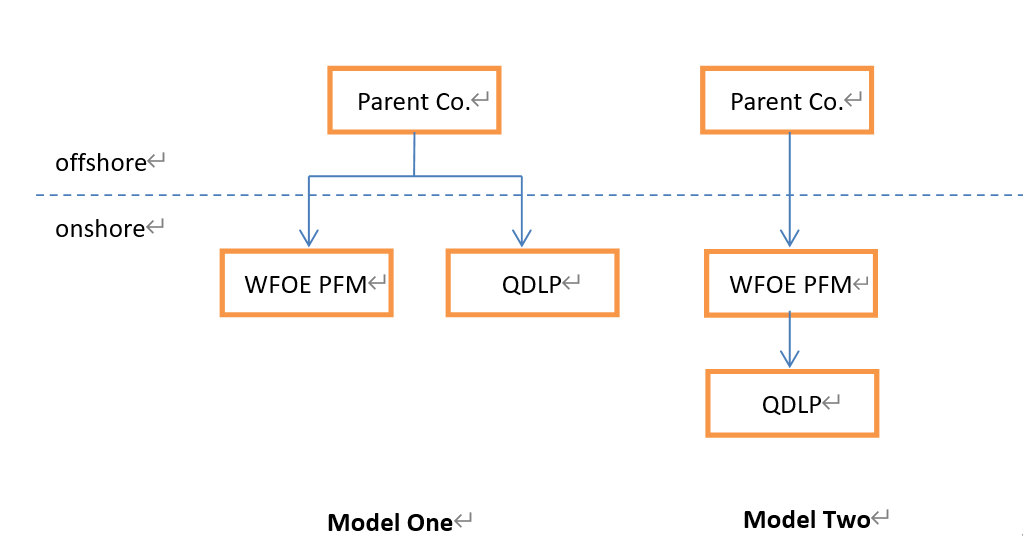

In addition to QDLP, some global asset managers have also set up wholly foreign owned private securities investment fund manager (“WFOE PFM”) in China to engage in domestic fund management business or other business.

According to applicable WFOE PFM registration guidance issued by AMAC, where a foreign institution has been doing QDLP business in China, the QDLP fund management business shall be properly segregated from other domestic private fund management business, the fund assets of any fund should be kept independently and should be held in custody individually, and appropriate measures to prevent conflict of interests should be adopted. Solely from the perspective of such requirements, we cannot conclude that the AMAC requires WFOE PFM and QDLP fund manager to be two separate legal entities. In practice, according to guidance by local financial regulator, WFOE PFM and QDLP fund manager shall be two separate legal entities at present. Therefore, currently there are mainly two holding structures in Shanghai in practice.

As far as we know, Shanghai no longer requires QDLP fund manager and WFOE PFM to be set up separately. Avoiding setting up two legal entities will help reduce cost and facilitate business operation, which is a positive development. However, one can only elect to be a private securities investment fund manager (applicable to WFOE PFM) or other private fund manager (applicable to QDLP fund manager) on the Asset Management Business Electronic Registration System (“AMBERS”) when applying for registration with AMAC, and according to the requirement on specialized operation (i.e., a private fund manager shall not engage in two or more types of private fund management business). Therefore, in practice, more issues need to be addressed with the help of local government and AMAC if a legal entity is to be both WFOE PFM and QDLP fund manager.

- Staffing Arrangement

Currently, the major business model of QDLP business is that QDLP funds will be invested in overseas funds under a feeder-master investment structure, which is relatively simple. Therefore, in practice, global asset managers should well consider the staffing arrangement before applying for QDLP license to reduce operation cost.

According to current rules by AMAC, a private fund manager shall be staffed with at least five employees; senior management personnel may not work concurrently for non-affiliated private fund managers or institutions doing business that is in conflict with the private fund management business, and senior management personnel other than the legal representative may not work concurrently for other institutions in principle, provided that if there are good reasons to have dual-hatting arrangement, the number of senior management personnel with dual-hatting arrangement shall not be more than 1/2 of all senior management personnel; no dual-hatting arrangement is allowed for employees other than senior management personnel. Considering that QDLP scheme is a pilot scheme, in practice, AMAC may allow more flexibility regarding the dual-hatting arrangement.

- Other Registration Issues

Such other requirements on capital, office and internal policies shall be met before the QDLP fund manager apply for registration with the AMAC. Furthermore, a legal opinion issued by a Chinese law firm shall be submitted to the AMAC as well.

Section 6 QDLP Fund Launching

QDLP funds are private funds. Therefore, all requirements on private funds shall be complied with when launching a QDLP fund, including such issues as private offering, investor eligibility, investor suitability, fundraising account supervision, AML and CRS. In addition, QDLP funds shall be filed with AMAC after fundraising and before investing.

- Types of QDLP Funds

Under the current setup of AMBERS, a QDLP fund may only be filed as a PE/VC fund or a securities investment fund, i.e., currently, the option of an “other investment fund” is not available for a QDLP fund.

- Wrapper Issue

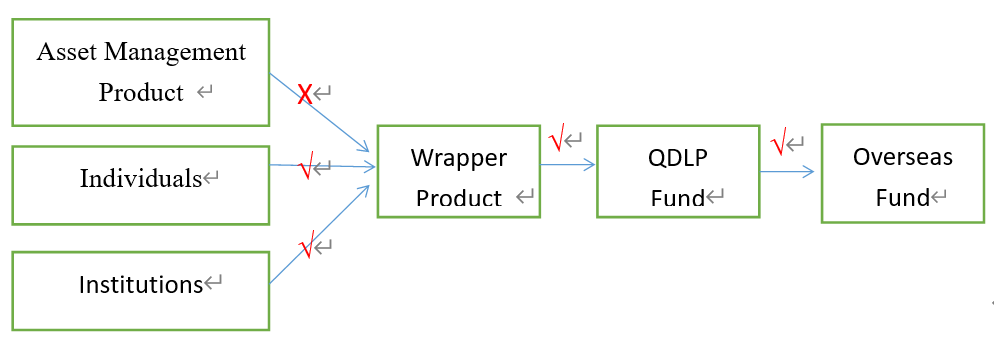

Most QDLP funds launched so far are not sold to end investor directly, and they are mostly sold to end investors through private fund managers, trust companies, securities companies, fund management company subsidiaries or other asset managers (“Wrapper Product Managers”). That is to say, a Wrapper Product Manager will launch a private asset management product (“Wrapper Product”), soliciting investment by end investors, and the Wrapper Product will then invest in the QDLP funds.

In order to address the multi-layer nesting issue in China’s asset management industry, in the Guiding Opinions on Regulating Financial Institutions’ Asset Management Business (“Guiding Opinion on Asset Management”) jointly promulgated by PBOC and other financial regulators in 2018, it is provided that an asset management product may invest in another layer of asset management product, provided that the latter must not further invest in other asset management products (except for public securities investment funds). Therefore, in the above-said investment structure, there shall be no asset management product as the investor of the Wrapper Product. However, overseas funds (both securities investment funds and PE/VC funds) to be invested by QDLP funds do not need to be counted in when considering the two-layer restriction.

- Difficulties with Wrapper Product and Wrapper Product Manager

After implementation of the Guiding Opinion on Asset Management, QDLP fund managers have met some difficulties when selecting Wrapper Product Manager. For example, according to implementing rules issued by CSRC, the private asset management products of securities companies and mutual fund management company subsidiaries generally shall comply with the double 25% investment concentration requirements (with few exceptions), namely a collective asset management product may not invest more than 25% of its net assets in a single property (e.g., any investment portfolio) and the amount invested in an asset by all the collective asset management products offered by the same manager may not exceed 25% of the asset. Therefore, it is quite difficult for securities companies and mutual fund management company subsidiaries to be Wrapper Product Manager anymore, and QDLP fund manager may explore more business opportunities with trust companies and other asset managers.

Section 7 Business Outlook

China investors have limited access to overseas financial markets, but they desire diversified asset allocation. As China is rapidly opening up its financial market to the world, we expect more development of QDLP business. According to recent policy dynamics, there will be more pilot districts and more foreign exchange quota, and QDLP scheme will be transformed from a pilot scheme into a full-scale program ultimately.

After implementation of the Guiding Opinion on Asset Management, financial regulators have broken the tradition of rigid payment. Many more Chinese investors (especially those high net worth investors) have well understood the risk investment concept and begun to actively participate in more investment programs.

QDLP fund manager may encounter some difficulties when they first entered the China market. However, with the QDLP scheme launched in 2012 and WFOE PFM initiated in 2016, many global asset managers have set up wholly owned asset managers in China, accumulated clients, built track record and gained some market reputation. All these will assist QDLP fund managers to address the fundraising issues. The industry has also been lobbying regulators for more favorable policies so as to attract more institutional investors.

* * * * * * *

Please kindly note that this Memo is rendered mainly with respect to local pilot QDLP rules as well as other relevant laws and regulations of the PRC (for purposes of this Memo only, the PRC does not include Hong Kong, Taiwan or Macau) in effect as of the date of this Memo. This Memo is being furnished solely to you on a confidential basis for your reference purposes only.

Jingtian & Gongcheng Investment Funds & Asset Management Group has vast experience with forming over 1,500 RMB, USD and hybrid funds in and outside of China, including successfully representing well over 20 global asset managers in applying for QFLP/QDLP/QDIE licenses/quota in Shanghai, Shenzhen, Beijing, Tianjin, Chongqing, Qingdao and other cities. Senior partner James Yong Wang has been a member on the Shanghai QDLP/QFLP panel for many years. Partner Eric Ye Zou is also a veteran in the field and has represented many international asset managers in QDLP/QDIE projects. In September 2019 and March 2020, Jingtian & Gongcheng received international recognition by garnering the China Investment Fund Law Firm of the Year Award from China Law & Practice and Asia Firm of the Year from The Asian Lawyer under leading international legal publishing group ALM, respectively.

Should you have any further questions, please feel free to contact Messrs. James Yong Wang and Eric Ye Zou below.